By Khaled Samirah

Khaled Samirah is a Senior Research Analyst at Euromonitor International.

The need for entertainment and e-learning at home was one of the main drivers for growth in the toys and games industry in 2020. Most product categories within video games and select categories in traditional toys and games, such as games and puzzles, outdoor toys and arts and crafts, all showed significant growth.

Although the overall growth of global traditional toys in 2020 was flat, the industry is expected to recover in 2021 and will return to positive growth. According to a report by Euromonitor International, traditional toys and games is expected to post a 2.5% CAGR in value, adding over USD11.5 billion in incremental sales over 2019-2024.

Four drivers for toys and games under COVID-19

Four key drivers have been shaping the industry’s performance under COVID-19, with some building on the trends that existed pre-COVID-19 and accelerating them in 2020.

Digitalization

Consumers are more inclined to purchase products that have digital capabilities, a trend that has been accelerated due to the pandemic and will likely be among the main factors of what consumers choose to purchase and enjoy. Video game products are also high in demand, with sales accelerated further due to COVID-19-driven hometainment and a shift towards virtual experiences.

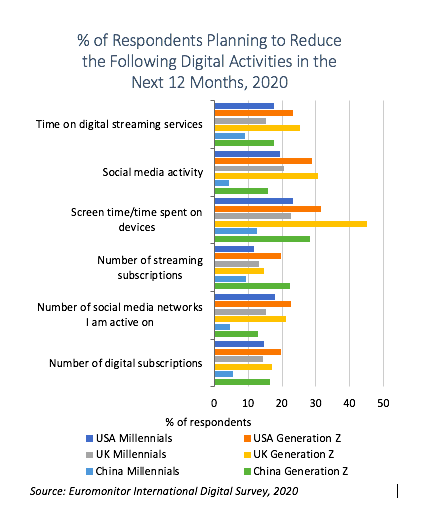

However, as work, social and entertainment interactions have shifted online for the majority of consumers in 2020, there is a clear risk of digital fatigue. Consumers across the world have begun showing an eagerness to return to physical sources of entertainment such as concerts and sports, in the search to reduce digital activities.

With increased return to physical life, developers, brands, services and entertainment properties will need to bring added value to virtual engagements, including enhanced capabilities, entertainment value, convenience, and authenticity of experiences rather than just an alternative to physical worlds.

Category Shifts

As consumers were forced to adapt to the pandemic, specific categories such as mobile and online games, scientific/educational toys, games and puzzles, and dolls and accessories all performed well in 2020. However, some categories, such as games and puzzles, will decelerate from 2021 onwards as stay-at-home orders and advisories are removed and consumers’ lives return to normal.

Licensing has also been an important driver of industry growth as entertainment venues and consumption patterns shift. 18–34 year-olds account for an increasing share of toy spending as they search for escapism, nostalgia and, potentially, investment. Established brands like Star Wars and Lego are favourites among more mature toy buyers, but licensing will also favour new players focusing on e-sports, YouTube stars and channels, and even anime.

Channel Shifts

The shift to online shopping and the e-commerce channel has been accelerated by the pandemic. Many small retailers struggled in 2020 due to closures and poor e-commerce logistics, while larger retailers like Amazon, Walmart and Target were not forced to close down and were able to continue capturing sales from others in the industry. As a result, many small independent specialist toy retailers face the possibility of permanent closures, leading to more retail consolidation across markets. This shift underscores the need for manufacturers and retailers to adopt robust omnichannel strategies to reach customers across platforms.

Macro Environment

Finally, many consumers have been placing more focus on value for money as they face financial uncertainties. They are looking for brands and products to deliver a meaningful experience, such as scientific toys that provide educational benefits. Those that fit in well between playtime, learning and future career development will be more in demand than other products.

2020 highlighted the need for robust omnichannel strategies to reach and retain customers. Successful retailers will compete by enhancing their sales and marketing strategies and adding new and exciting shopping methods to their omnichannel strategies.