I am very pleased to publish an outstanding report on the ongoing supply chain crisis by Bob Moog, Chairman of AreYouGame.com.

ABOUT THE AUTHOR

Robert Moog, Chairman of AreYouGame.com

A. Robert Moog is a 36 year veteran of the toy industry. He originally sourced factories in China in the early 1990s and has worked with more than two dozen different factories in the US, Canada, Thailand,

China, Hong Kong, and India. In 1985 Mr. Moog co-founded University Games, a leading global game and puzzle manufacturer. In 1999 Mr. Moog founded AreYouGame.com, an e-commerce retailer and private label producer. AreYouGame carries more than 3500 different games/puzzles and STEAM products and works with more than 125 different suppliers. Currently, Mr. Moog is researching the systemic changes in the consumer products industry and the strategic challenges facing global companies in the next 10 years.

Mr. Moog has lectured at Golden Gate University on entrepreneurship and strategic marketing. He has also served as a guest speaker at several universities including the University of San Francisco and Stanford University.

EXECUTIVE SUMMARY

The current supply chain issues require a resetting of the risks and the responsibilities of the three major players in the supply chain: foreign factories, US, Canadian and European suppliers, and retailers. To maximize retail performance in the short term (2021-2022) and the long term, all three business groups need to modify how they think about their interrelationships. The Modern Retailer will benefit by proactively seeking strategic partners who are willing to find more dials and knobs to turn to find success. Without some risk adjusting and some modifications to how all three groups conduct business, consumer products will not be on shelves at reasonable prices for the 2021 and 2022 holiday seasons.

The US and Canada are now experiencing the third consecutive year of unprecedented threats to the supply chain that brings consumer products from Chinese factories to the nation’s retail stores. In the toy industry, for example, more than 80% of the $26 billion in toys, games, and puzzles that form the US toy industry are manufactured in China. These shipments are being delayed to the point of putting the Christmas selling season at risk.

First, in 2019, protective tariffs increased the cost of bringing toys into the United States. While some toy makers increased costs to retailers, most suppliers absorbed the impact of the tariff and experienced margin erosion. The threat of additional tariffs on games/puzzles paired with China’s reaction to the tariffs increased anxiety and uncertainty in 2019. Then starting in March 2020 the Coronavirus pandemic delayed factory production, reduced traffic flow of containers, and resulted in port slowdowns as the Covid 19 virus spread throughout the factories, the ships, and the port personnel. Finally, in 2021, the increase in freight charges (which increased more than 400% from January 1, 2021-July 15 2021) has completed the trifecta of supply chain dysfunction.

All of this has been hashed and rehashed, but interestingly little has been said about how companies should deal with the situation. What are the solutions? In this paper, we explore why this is happening, how various stakeholders have reacted, and what retailers can do to have a successful 2021 and avoid empty shelves during the holiday season.

IMPACT OF CONTAINER INCREASES

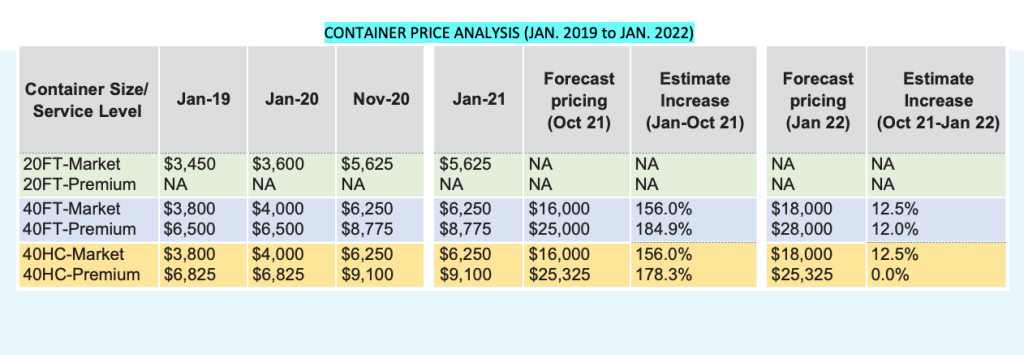

The impact of freight rate increases varies based on the number of units in the container and the overall cost of the individual units. However, both large items that are expensive and small items that are lower priced are significantly impacted when container prices increase 200% in an 18 month period. For example, a typical board game box (10.5″ X 10.5″ X 2.5″) will fill a 40 ft container with about 10,000 games. At January 2020 rates ($4000) that is about $.40 per unit. However, at estimated October 21 rates the same 40 ft container will cost $25,000 (must ship Premium rates) which equals $2.50 per unit. The increase of $2.10 per game if fully passed on to the retailer will result in a game that retails for $19.99 being increased to $24.99-$29.99. Raising rates of games and toys this much will result in lower sales as consumers move to substitute with other choices–hurting the entire industry.

WHO IS GETTING SHIPMENTS SHIPPED?

Short answer: Only those who are paying 3-4 X normal shipping rates and booking Premium. The normal (Prior to 2020) system for shipping products from China was fairly straightforward if not completely fair and transparent. Companies booking freight had three ways to book:

- Negotiated Shipping Rates: These were typically large shippers (Nike, Gap, Apple) or retailers who imported directly (Walmart, Target, MarMaxx, Kohls) where annual negotiated rates were established each year. These rates typically ran 20-30% below market rates.

- Market rates/Spot rates: These rates fluctuated during the year based on fuel prices and seasonal demand. Shippers of less than 1000 containers per year typically shipped at these rates.

- Premium Rates: These preferred rates were for faster shipping and guaranteed that bookings would not be bumped.

In 2021 with rates increasing monthly and running 200% or more ahead of 2020 rates those companies booking negotiated rates or market rates are finding their bookings postponed by weeks or months. The demand for Premium rates is so high that the shipping companies are often refusing space to long-time and large customers who have booked under lower rates. This threatens the economic model and the sustainability of large companies, national retailers, and smaller suppliers who cannot get their products shipped in a timely manner. In order to have product at retail in 2021 and 2022 suppliers and retailers must be proactive in addressing the situation together and forging creative solutions.

WHY IS THE SUPPLY CHAIN BROKEN?

While the container flow is out of balance along with shortages of chassis at port and drivers for trucks, these are only symptoms of a larger supply chain dysfunctionality. It isn’t these events that have caused the major supply chain issues, but rather the reaction of factories, suppliers, and retailers that have brought us to the brink of insufficient supply of product and double-digit price increases. These exogenous events have been met by three primary and distinct reactions. Each is indicative of a Company’s culture and decision-making process.

- THE POSTPONER: Taking the current increased freight rates as an example, many suppliers and some retailers decided in January and February to “wait and see” if the rates went down in July or August. The thinking was similar to the way some people think about “overvalued” stocks. Since freight rates were at unprecedented high levels these companies decided to wait until freight rates reverted back to “normal” levels. To accept the higher rates would negatively impact gross margins. To the “Postponer” it only made sense to wait and avoid excessive freight charges.

- STATUEMAN/STATUEWOMAN: These managers understood that there were threats to profitability but weren’t given

any direction to change course by upper management. Without direction from senior executives, they continued to manage their business as they had in prior years expecting the supply chain to self-correct by Q4. These buyers used language like “hope” and “let’s cross our fingers” but have not actually adapted to the reality of supply chain disruptions. They continue to fight any cost increases or changes in terms of payment without offering much to assist the suppliers or the factories. By the time many start scrambling for temporary space or to fill planograms they are finding few suppliers prepared.

- PLANNER: These decisionmakers are more comfortable with risk than the other two groups. They have consistently worked directly with their Chinese factories to understand the entire supply chain from forest/mill to retail Distribution Center. They have modified their inventory management systems and worked to modify terms and timing with their customers. They will be able to build their businesses with those retailers who are willing to adapt to the realities of today’s supply chain. For retailers who take the “PLANNER” approach, the holiday season as well as 2022 will be less stressful and more profitable.

We have not explored how the percentages of the three types of managers breaks out, but it appears that most of Suppliers in the Toy Industry are POSTPONERS (type 1) and most of the retail buyers are STATUEMAN (type 2). Unfortunately, both of these paths have proven to have devastating effects. Meanwhile the PLANNER-style managers are having record years and are better ready for Q4 2021 than their competitors and customers. It is imperative to understand “what is happening” in order to forge a plan of action for your Company. The seminal roots of the problem can be seen in the very basic way that toys are made, warehoused, and ordered.

A LITTLE HISTORY

In manufacturing and operations management there are three basic ways of building and controlling inventory:

Batch manufacturing, continuous flow, and just-in-time manufacturing. In the 21st century, a natural disharmony has developed in many consumer products categories including the toy industry that need to be addressed during the current situation.

BATCH MANUFACTURING (The Factory)

Factories in China required Minimum Order Quantities (MOQs) in order to manufacture a toy, puzzle or game. The quantities generally run from 10,000-25,000. These are manufactured in one production run and shipped complete to the US supplier or are offered on an FOB basis direct to retailers.

BATCH IN/JUST IN TIME OUT MODEL (The Supplier)

The US supplier creates a flow of inventory so that there is a stilted continuous flow. The goal of good inventory management is to bring in the next shipment when the current inventory is down to one month’s inventory level. The amount brought in is the batch built by the factory. Once received the inventory can be stickered, assorted, or bundled as required by various retail customers. This Batch in/Just-in-time out across many items creates a staggered system where various items come in every month as the inventory levels run down.

JUST IN TIME SYSTEM (The Retailer)

Retailers, on the other hand, are working on a Just-in-Time system where their goal is to order weekly

and keep 6-8 weeks of inventory in their distribution system at all times. If volume increases or decreases retailers like Walmart and Target adjust their purchases on a weekly basis. Since the Chinese factories manufacture and ship by batch and the retailer orders only what they need each week, the bulk of the inventory risk falls on the Supplier. Normally, this is a manageable although not efficient system for all parties. In 2021 this is not working since the Suppliers are not maintaining a continuous flow and may not be in a financial position (after surviving 2019 and 2020) to handle the financial risk of the “system.” The result is late shipments, missed modular sets, strained relationships, and increased costs across all three elements of the supply chain. To fix this short term for 2021 and 2022 a rejuggling of risk and a modification in how retailers work with suppliers and suppliers work with factories, is required.

WHAT TO DO?

There is not a simple cure-all to the situation but the Retail Manager may be the key to solving the situation. Generally, the retailer (national chains) has the most resources in terms of people, capital, and cash flow.

However, it is the retailer that takes the smallest inventory risk and takes the longest amount of time to pay for the product. The factory makes a smaller margin but generally is paid the fastest with terms ranging from pre-payment to 30 days from bill of lading. The Supplier is financing the inventory with 30-90 day payment terms to the retailer. In addition, labor increases and freight increases in 2020 and 2021 have been absorbed by the Supplier in most cases, resulting in substantial margin compression. The reaction of the Supplier has depended on whether they are a Postponer, Statueman, or Planner—but none of the reactions fully supports The Retailer. While all three players in the chain need to make modifications, the flexible and pro-active retailer will gain the most by adapting to the changing business environment.

By understanding what is happening in terms of management philosophy, factories, suppliers, and retailers can all be successful both in the short term (2020-2021) and the long term. The changes needed will not only improve performance during the current crisis but establish internal practices that will benefit the players during the structural retail changes of the next ten years. Sitting still and staying the course is a dangerous path and may lead to a slow, long decline for all parties.

The MODERN RETAILER

RETAILERS: Take an audit of your suppliers. Who are the POSTPONERS, STATUEMEN/STATUEWOMEN, and who are the PLANNERS? Create a strategic initiative with the PLANNERS and work out a 2-year plan with them that accomplishes the following:

- Maintains product flow-This is essential.

- Allows your company to maintain a blended margin that is acceptable to management.

- Creates differentiation in supplier management from others in the market place It is important for the Modern Retailer to take a revised look at supplier management. It requires the grit to identify and trust some suppliers to give you preferential treatment to the Planner-style suppliers and to deliver high quality products and programs. To strike the correct balance orders may need to be placed earlier, commit more space to the Supplier and blend margins with higher and lower margin product mixes. The key is to develop a scenario where you “know” that you will get product delivered. This is the most important objective.

The Modern Retailer

All of these tactics shift some risk from the Supplier to the Retailer, but they may actually create a more functional supply chain than the current structure. These changes also shift more of the control from the Supplier to the Retailer, as they are aimed to increase the likelihood of timely delivery and margin maintenance. Each Retailer, Supplier, and Factory needs to find the right formula for them. The key is that until senior executives instigate and implement some changes to their thinking about the supply chain, we will see increasingly empty shelves and higher Retail prices to the consumer.

ACTION PLAN

The Modern Retailer

A. Offer Supplier Incentives and Penalties: Retailers may offer reverse-incentives for 100% shipping

compliance by actually paying more. Some retailers are providing extra ads or guaranteeing promotional space for suppliers that ship 100% complete. Tied to the incentive for 100% complete shipments is a

penalty for less than 90% shipping compliance. These retailers are allowing Suppliers to opt in to these programs.

B. Shorter Payment Terms: Retailers are offering to pay in 30-day terms with an early payment discount. This is a win for the Retailer since it both reduces costs and increases the likelihood of delivery.

C. Sliding Pricing Scale: Another idea is to create a sliding pricing scale for the Retailer that is indexed to freight costs. While this shifts cost risk to the Retailer if properly designed it can also lead to a reduction in costs when freight rates are reduced. Without this fulcrum, Retailers may see cost increases in 2021 which become permanent even if freight costs are later reduced.

D. Technology/Business Analytics: Retailers, Suppliers, and Factories will benefit from exploring technology solutions that facilitate better supply chain management from purchase order to delivery.

The Opportunist Supplier

Suppliers play a role in bringing the supply chain back in balance. The recipe for suppliers requires creatively modifying relationships with factories and with retail customers. Suppliers can work with Factories to provide forecasts by item annually and agreeing to accept shipments when the factory manufactures, regardless of time of year. Suppliers can try and be more flexible on annual raw material purchases and in the specifications on commodity items like paper and plastics.

Suppliers can also be proactive with Retailers and work with Retailers to anticipate their needs. This may require more planning meetings vs selling meetings with key customers so that lead times can be better managed. Suppliers need to be margin conscious regarding their Retail customers and plan price increases with longer notice periods (90 days or more). By working more closely with Retailers on issues that Retailers are facing, this period can be a hugely successful time for Suppliers vs. the nightmare that they might be facing today.

The Factory

Factories will benefit by better and more complete communication with their Suppliers. When Suppliers understand the raw material constraints, the labor constraints, and the space constraints of factories, they can be better customers. For the factories providing longer lead times, utilizing Chinese contacts, and proposing cost and time efficiencies will be met with sincere approval by Suppliers who are PLANNERS.

CONCLUSION

The focus of the Supply Chain Crisis is on the Covid outbreaks, freight rates, transportation shortages, port capacities, and labor shortages. However, the underlying framework of how factories, suppliers, and retailers work together currently creates more dysfunction and product shortages than are necessary. By planning together, changing the timing and terms of working together, and by adjusting the inventory risk through innovative and creative programs Retailers can be more successful. Suppliers and Factories can also deliver better results in 2021 and 2022 by rethinking how they interact with their customer base.